Many property managers assume that any cleaning company showing up with a logo on their van is properly covered. That assumption is costly. Insurance requirements for commercial cleaning vary by state, facility type, and contract size, and the gaps between what a vendor claims to carry and what they actually hold can expose your building to six-figure liability. This guide breaks down exactly what insured cleaning means, which policies matter most for offices, retail centers, and healthcare facilities, and how to verify coverage before a single mop hits your floor.

Table of Contents

- What is an insured cleaning service?

- Core insurance policies and what they cover

- How insured services protect your property and business

- Industry standards and contract essentials for insured cleaning

- Advanced coverages, common exclusions, and best practices

- Insured cleaning: What most property guides never warn you about

- Partner with a fully insured cleaning team

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Not all cleaners are fully insured | Insist on documented, up-to-date coverage to protect your property and reputation. |

| Minimum insurance isn’t enough | Higher limits and specialized policies are needed for healthcare, retail, and high-rise cleaning contracts. |

| COIs must list you as additional insured | Only a current certificate with your company named provides the highest risk protection. |

| Bonds supplement, not replace insurance | Janitorial bonds cover theft, but do not substitute for liability or workers’ compensation. |

| Contract details matter | Include clear insurance requirements in every service contract for legal and financial safety. |

What is an insured cleaning service?

An insured cleaning service is not simply a licensed business. It is a company that holds specific, active insurance policies designed to protect you, your tenants, and your property from financial loss if something goes wrong during a cleaning job. A business license proves a company is legally registered. Insurance proves it can actually pay when damage or injury occurs.

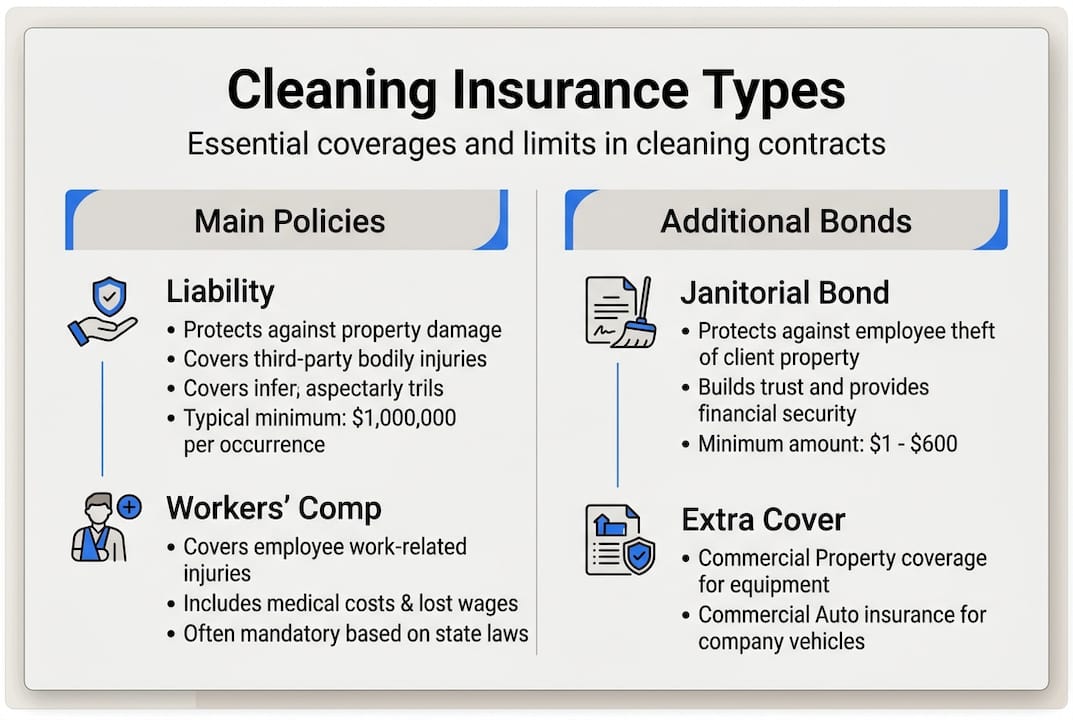

Core insurance types include general liability, workers' compensation, and janitorial bonds. Each one covers a different kind of risk:

- General Liability: Covers third-party bodily injury or property damage caused by the cleaning crew. If a cleaner knocks over a display case in a retail store, this policy responds.

- Workers' Compensation: Covers medical costs and lost wages if a cleaning employee is injured on your property. Without it, you could be held liable for that worker's injuries.

- Janitorial Bond: A surety bond that protects you from theft by cleaning staff. It is not insurance, but it fills a specific gap that standard liability policies leave open.

Missing even one of these three protections leaves a real hole in your risk management strategy. Property damage claims related to cleaning incidents typically range from $5,000 to $50,000 per event.

Many cleaning companies carry only a basic general liability policy and call themselves insured. That is technically true, but dangerously incomplete. Enterprise office buildings, medical suites, and retail centers often require all three coverage types plus documented proof. If your current vendor cannot produce that proof, your commercial cleaning overview standards may not be met, and you could be absorbing risk you never agreed to carry.

Core insurance policies and what they cover

Knowing the labels is one thing. Understanding what each policy actually does in practice is what helps you spot incomplete coverage before an incident occurs.

General Liability is the foundation. Most commercial cleaning contracts require a minimum of $1 million per occurrence and $2 million in aggregate. Higher-risk environments like hospitals or high-rise lobbies often push that requirement to $5 million. This policy covers property damage and third-party injuries, but it does not cover damage to property the cleaner is actively working on. That distinction matters more than most managers realize.

Workers' Compensation is mandatory for cleaning employees in nearly every state. Workers' comp rates run roughly $3 to $8 per $100 of payroll under NCCI classification codes 9014 and 9015, which are specific to janitorial work. If a cleaning firm skips this coverage to lower their bid, and a worker is hurt on your site, you may face direct legal exposure.

Janitorial Bonds are frequently misunderstood. They are not a replacement for liability coverage. They exist solely to compensate clients if a cleaning employee steals from the property.

Enterprise and healthcare contracts require higher liability limits and certificates of insurance (COIs) naming you as an additional insured. This is non-negotiable in most institutional leases.

| Coverage type | What it covers | Typical minimum limit |

|---|---|---|

| General Liability | Property damage, third-party injury | $1M per occurrence |

| Workers' Compensation | Employee injury, medical costs | State-mandated |

| Janitorial Bond | Employee theft | $10,000–$100,000 |

Pro Tip: Never accept a verbal confirmation of coverage. Always request a certificate of insurance directly from the insurer, not the vendor. It takes one call to verify, and it can save you enormously.

Understanding these details also helps you evaluate insurance standards in California and other states where minimums differ. Cleaning vendors that reduce manager liability through proper coverage are worth the slight premium in their rates.

How insured services protect your property and business

Let's walk through what actually happens when an incident occurs on your property during a cleaning shift.

A cleaning crew uses an industrial chemical to strip and refinish a lobby floor. The solution reacts with the existing tile coating and damages $20,000 worth of flooring. Without a COI listing you as additional insured, you are negotiating with the cleaner's insurer as a stranger. With it, you have direct rights to that policy, and the claim moves quickly.

Property damage claims from cleaning average $5,000 to $50,000, and comprehensive coverage costs a small cleaning firm between $320 and $675 per month. That monthly cost is relatively modest. When you see an unusually low cleaning bid, ask yourself how the vendor is keeping costs down. Underinsurance is a common answer.

Here is a step-by-step process for handling a cleaning incident on your property:

- Document the damage immediately with photographs and written notes.

- Notify the cleaning company in writing the same day.

- Request the active COI and verify that your company is listed as additional insured.

- Contact your own property insurance carrier to report the event.

- File a third-party claim directly against the cleaner's liability policy.

- Follow up with a written incident report kept in your vendor file.

Coverage requirements tend to be highest in building entranceways, medical suites, and food-service areas, because these zones carry the greatest risk of injury or contamination. If you manage insured cleaning services in Massachusetts or similar regulated states, your lease language may already mandate specific policy minimums. For other property risk scenarios, the same principle applies: documented coverage beats verbal assurances every time.

Industry standards and contract essentials for insured cleaning

A vendor saying "we're fully insured" in a sales meeting is not a contract clause. You need specific language in every cleaning agreement that locks in the protection your facility requires.

When issuing a request for proposal (RFP), require the following from every bidder:

- A COI listing your company as additional insured on all active policies

- A waiver of subrogation preventing the vendor's insurer from suing you after paying a claim

- Written verification of general liability, workers' comp, and bond limits

- Policy expiration dates and insurer contact information

- Notice of cancellation clause (usually 30 days written notice to you)

Enterprise contracts mandate additional insured status, waiver of subrogation, and proof of insurance as standard terms. If a vendor resists any of these, that is a red flag.

Healthcare facilities often go further, requiring pollution liability endorsements that cover chemical exposure or biohazard incidents. Office properties in major markets typically demand $2 million to $5 million in general liability from cleaning vendors. Retail centers with heavy foot traffic fall somewhere in between, but should not settle for bare minimums.

Refer to contract cleaning standards and facility cleaning compliance resources for state-specific guidance. Warning signs of missing protections include unsigned indemnification clauses, no bond documentation, and COIs that list the vendor rather than your entity as the certificate holder.

Advanced coverages, common exclusions, and best practices

Standard general liability policies contain an exclusion that catches many property managers off guard: the care, custody, and control exclusion. It means that if a cleaner damages the specific item they were actively cleaning, the standard GL policy will not pay. A cleaner who scratches a marble countertop while polishing it falls into this gap.

To fill it, look for inland marine insurance or a care, custody, and control endorsement on the vendor's policy. Edge cases like these also include healthcare pollution risk and elevated workers' comp rates for high-rise window cleaning work.

Additional coverages worth knowing:

- Pollution Liability: Required in most healthcare settings for chemical and biohazard exposure

- Inland Marine / Equipment Floater: Covers cleaning equipment and client property in the vendor's control

- Umbrella Policy: Extends coverage above standard policy limits, often needed for large commercial contracts

- Employment Practices Liability: Increasingly requested in enterprise cleaning contracts

Best practice is to have your legal or insurance advisor review the vendor's full policy documents, not just the summary COI. The certificate shows limits. The actual policy shows exclusions.

Pro Tip: Require updated COIs every year and log the renewal dates in your vendor management system. Policies lapse, and a gap of even a few days can leave you exposed.

For high-risk settings, review best practices in Florida and other states with elevated cleaning risk profiles. Also consider the property protection tips applicable to exterior and seasonal hazards that sometimes overlap with cleaning vendor responsibilities.

Insured cleaning: What most property guides never warn you about

Here is the uncomfortable truth most insurance checklists skip: collecting a COI is not the same as being protected. A certificate shows the policy existed on the day it was issued. It does not guarantee the policy is still active, that the limits are sufficient for your specific facility, or that the vendor did not quietly change insurers after sending you the document.

Some vendors offer below-market pricing by carrying only the legally minimum bond while skipping full general liability or dropping workers' comp mid-contract. You hire them thinking you have coverage, and then an incident reveals the gap. At that point, the financial exposure lands on you.

The harder truth is that the cheapest cleaning bid in your stack is often cheap because someone is underinsured. Bad incidents in underinsured relationships damage more than property. They damage tenant trust, complicate lease renewals, and occasionally generate lawsuits that drag on for years.

Make insurance verification a repeatable, audited process. Pull COIs annually, call the insurer to verify active status, and document every step. That is not excessive caution. That is property management done right.

Partner with a fully insured cleaning team

If you want to eliminate insurance uncertainty from your vendor relationships, working with a team that treats compliance as standard practice is the simplest path forward.

At Sparkle Pro Commercial Cleaning, we carry full general liability, workers' compensation, and janitorial bonds across every market we serve. We provide COIs before any project starts, and we list your company as additional insured as a default. Whether you manage properties in California or need a New York insured team, we are ready to show you our documentation first, then start work. See our full insured cleaning services and request your COI review today.

Frequently asked questions

What types of insurance must a commercial cleaning company carry?

A reputable commercial cleaning company should carry general liability, workers' comp, and a janitorial bond to provide full protection for property managers and building owners.

How much does insured cleaning coverage cost?

A small cleaning firm typically pays $320 to $675 per month for comprehensive coverage, a cost that gets built into their service rates.

What proof of insurance should I request from a cleaning service?

Always request a COI that lists your company as additional insured, along with verification of policy limits and current expiration dates directly from the insurer.

Are janitorial bonds the same as insurance?

No. Janitorial bonds cover employee theft only and do not replace general liability or workers' compensation insurance.

Why do healthcare or high-rise facilities require extra coverage?

Healthcare and high-rise environments carry elevated chemical and physical risks, so they require pollution liability and higher workers' comp limits beyond standard commercial policies.

Recommended

- Decode commercial cleaning terms: guide for managers

- Sparklepro Commercial Cleaning

- Streamline Your Commercial Floor Cleaning Process

- Top examples of janitorial services for every facility type

- Insurance benefits of leak detection: California guide

- Why hiring contractors reduces cost and risk for property managers