Insured cleaning companies are defined as professional cleaning providers that carry verified general liability insurance, workers' compensation, and bonding coverage, making them the only defensible choice for property managers and business owners who cannot afford uncovered liability. When a cleaner slips on a wet floor in your facility, or a piece of equipment damages a tenant's property, the financial exposure lands directly on you without proper coverage in place. Understanding why choose insured cleaning companies is not a formality. It is a core risk management decision that determines whether an incident becomes a minor claim or a six-figure legal problem. This article breaks down the coverage types, verification steps, and real advantages that separate insured providers from uninsured alternatives.

What types of insurance do insured cleaning companies carry?

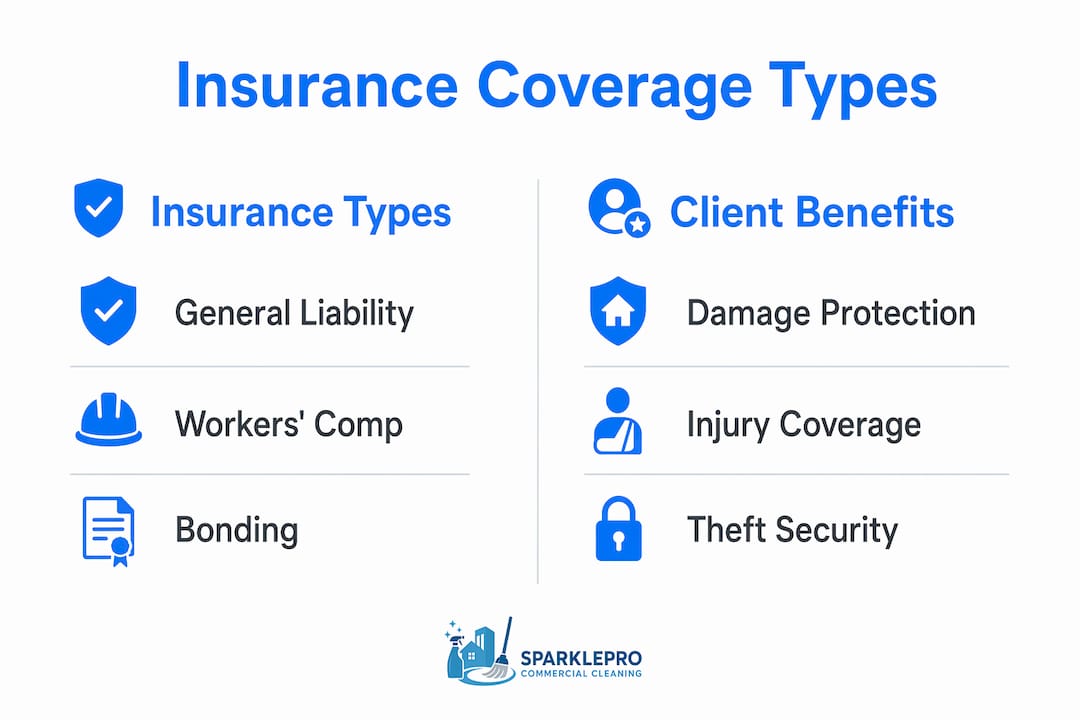

Insured cleaning companies typically carry four distinct coverage types, each addressing a different category of risk that property managers face during routine facility maintenance.

General liability insurance covers accidental property damage and third-party bodily injury. If a cleaning crew knocks over a server rack or a visitor trips over a mop bucket, general liability pays for repairs, medical costs, and legal defense. This is the foundational policy and the first document you should request from any provider.

Workers' compensation is a no-fault system that covers medical treatment and lost wages if a cleaning employee is injured on your property. Workers' comp coverage removes the property owner from the dispute entirely, since benefits flow directly from the insurer to the injured worker. Without it, an injured cleaner could pursue a claim against your facility.

Bonding, also called employee dishonesty coverage, protects you against theft or fraudulent acts by cleaning staff. A bonded company has a surety bond that pays out if an employee steals equipment, cash, or tenant property. This matters especially in multi-tenant office buildings and healthcare facilities where access to sensitive areas is unavoidable.

Commercial auto insurance covers any vehicle used during cleaning operations, including vans carrying equipment to your site. A collision involving an uninsured cleaning vehicle on your property can create liability questions that take months to resolve.

Many established providers bundle general liability, commercial property, and business interruption coverage into a Business Owner's Policy (BOP), which signals financial maturity and operational seriousness.

- General liability: covers property damage and third-party injury

- Workers' compensation: covers on-site worker injuries without employer dispute

- Bonding: covers theft or dishonest acts by cleaning employees

- Commercial auto: covers vehicle incidents during service delivery

- BOP: bundles core coverages into one policy for broader protection

Pro Tip: Ask for the declarations page of each policy, not just the certificate summary. The declarations page shows exact coverage limits, exclusions, and endorsement numbers, giving you a complete picture of what is actually covered.

How to verify a cleaning company's insurance coverage

Verification is where most property managers make their biggest mistake. Transitioning from verbal assurances to documented proof is the single most effective step you can take to protect your facility from uncovered claims.

Follow this process before signing any cleaning contract:

- Request the Certificate of Insurance (COI). The COI is a standardized ACORD 25 form that summarizes the provider's active policies. Ask for it before the first site visit, not after.

- Check effective dates and policy limits. Confirm that coverage is active for the full duration of your contract. A policy that expires mid-contract leaves you exposed from that date forward.

- Understand COI limitations. A COI is a snapshot, not a guarantee. It confirms coverage existed at the time of issuance but does not automatically extend protection to you as a client.

- Require additional insured endorsements. Without an endorsement, the cleaning company's policy covers the company, not you. Contracts should specify endorsement forms CG 20 10 or CG 20 37, which legally extend coverage to your organization as an additional insured.

- Call the insurer directly. Requesting the COI directly from the insurer eliminates the possibility of a falsified or outdated document. Ask the insurer to confirm policy status, limits, and whether cancellation notices will be sent to you.

- Set a calendar reminder for renewal. Policies renew annually. Build a compliance calendar that flags COI expiration dates 60 days in advance so you can request updated documentation before coverage lapses.

| Verification step | What it confirms |

|---|---|

| Request ACORD 25 COI | Active policies and coverage types |

| Check effective dates | Coverage is valid for your contract period |

| Confirm additional insured endorsement | Your facility is legally covered under their policy |

| Call insurer directly | Policy is current and not subject to pending cancellation |

| Review policy limits | Coverage amounts are adequate for your facility's risk profile |

Pro Tip: Build a subcontractor coverage checklist into your vendor onboarding process. Treating COI collection as a recurring compliance task, rather than a one-time box to check, closes the gaps that lead to costly surprises.

What advantages do insured companies offer over uninsured providers?

The financial and legal gap between insured cleaning companies and uninsured alternatives is wider than most property managers realize until something goes wrong.

Uninsured independent cleaners expose clients to employer liability and injury risks that the property owner absorbs entirely. If you hire an uninsured individual and they are injured on your property, you may be classified as a de facto employer under state labor law, triggering workers' compensation obligations and potential lawsuits. That exposure does not exist when you hire a properly insured company.

There are also tax and legal classification risks. Paying an uninsured independent cleaner without proper contractor documentation can trigger IRS scrutiny around worker misclassification. The cost savings from a lower hourly rate evaporate quickly when weighed against potential back taxes, penalties, and legal fees.

The table below illustrates the core differences:

| Factor | Insured cleaning company | Uninsured independent cleaner |

|---|---|---|

| Property damage liability | Covered by provider's general liability | Falls on property owner |

| Worker injury liability | Covered by workers' comp | May fall on property owner |

| Theft protection | Covered by bonding | No protection |

| Legal dispute resolution | Handled through insurer | Direct legal exposure for owner |

| Tax/classification risk | Low, clear contractor relationship | High, potential misclassification |

Beyond liability, insisting on documented insurance shifts financial responsibility from your organization to the cleaning provider in the event of any incident. That shift is the entire point of the arrangement. A provider unwilling to supply insurance documentation is signaling that the risk stays with you.

The advantages of hired cleaning services from insured providers also extend to dispute resolution. When damage occurs, a claims process through a licensed insurer is faster, more structured, and less adversarial than pursuing an uninsured individual through small claims court or civil litigation.

How does insurance connect to service quality and accountability?

Insurance is not just a legal formality. It is a proxy for how a cleaning company operates internally. Insured cleaning companies tend to prioritize training, safety protocols, and professional standards because their insurance premiums and renewability depend on maintaining a clean claims record.

A company that has invested in general liability, workers' comp, and bonding has also invested in the administrative infrastructure to manage those policies. That infrastructure includes employee screening, safety training, incident reporting procedures, and supervisory oversight. These are the same processes that produce consistent, high-quality cleaning outcomes for your facility.

Consider the contrast: an uninsured cleaner has no external accountability mechanism. An insured company answers to its insurer, its clients, and its own compliance requirements simultaneously. That layered accountability produces measurably better behavior on-site.

The benefits of insured cleaners also include reputation protection for your own organization. If a cleaning incident at your facility becomes a legal matter, having a fully insured vendor on record demonstrates due diligence. Risk managers, insurance auditors, and legal counsel all look for documented vendor compliance when evaluating your exposure.

Long-term partnerships with insured providers also reduce operational friction. You spend less time managing incidents, chasing documentation, or replacing vendors who cannot meet basic compliance standards. The importance of licensed cleaning companies compounds over time as your vendor relationships mature and your facility's risk profile improves.

Key takeaways

Choosing insured cleaning companies is the most direct way to transfer liability risk away from your facility and onto a provider equipped to manage it.

| Point | Details |

|---|---|

| Insurance types matter | General liability, workers' comp, bonding, and commercial auto each cover distinct risks. |

| COI alone is not enough | Additional insured endorsements (CG 20 10 or CG 20 37) are required to extend coverage to your facility. |

| Uninsured providers shift risk to you | Property damage, worker injuries, and theft exposure fall on the property owner without proper coverage. |

| Verification must be ongoing | Set calendar reminders to renew COI documentation before policies lapse each year. |

| Insurance signals service quality | Insured companies maintain training and safety standards that directly improve cleaning outcomes. |

What I've learned from years of watching property managers get this wrong

The most common mistake I see is treating insurance verification as a one-time task at contract signing. A property manager collects the COI in January, files it, and never looks at it again. By October, the policy has lapsed, the cleaning company hasn't mentioned it, and the facility is operating with zero coverage. When an incident happens in November, the claim gets denied and the property owner is left holding the bill.

The second mistake is accepting a COI without confirming the additional insured endorsement. I have reviewed dozens of vendor files where the COI looked perfect on paper but the endorsement was missing. A COI without endorsements is a document that protects the cleaning company, not you. That distinction matters enormously when a claim is filed.

What actually works is treating COI management the same way you treat lease renewals or fire inspection schedules. It goes on the compliance calendar. It gets a 60-day advance notice. It gets confirmed with the insurer directly, not just with the vendor. That process takes about 20 minutes per vendor per year and eliminates the single largest source of uncovered liability in facility maintenance.

The deeper point is this: a cleaning company that resists providing documentation, delays sending endorsements, or gets defensive about insurance questions is telling you something important about how they operate. Trustworthy cleaning services make this process easy because they have nothing to hide and everything to gain from a long-term client relationship.

For property managers who want a practical starting point, the property manager's hiring guide from Sparkleprocommercialcleaning covers the full vendor vetting process in detail.

— Sales

Work with a fully insured commercial cleaning partner

Sparkleprocommercialcleaning carries verified general liability insurance, workers' compensation, and bonding coverage across all service areas, and provides COI documentation and additional insured endorsements before any work begins. Property managers and business owners working with Sparkleprocommercialcleaning get the liability protection and compliance documentation their facilities require, without the back-and-forth that slows down vendor onboarding. Whether you manage office buildings, retail centers, or healthcare facilities, Sparkleprocommercialcleaning's insured cleaning services in Massachusetts and across the country are built to meet your compliance standards from day one. Contact Sparkleprocommercialcleaning to request your COI and get a quote for your facility.

FAQ

What does it mean for a cleaning company to be insured?

An insured cleaning company carries active general liability insurance, workers' compensation, and bonding, which collectively cover property damage, worker injuries, and employee theft during cleaning operations.

Why is workers' compensation important when hiring a cleaning company?

Workers' compensation is a no-fault system that pays medical and wage benefits to injured cleaning employees directly, removing the property owner from legal and financial liability for on-site injuries.

What questions should I ask cleaning companies about their insurance?

Ask for the ACORD 25 Certificate of Insurance, confirm additional insured endorsement forms CG 20 10 or CG 20 37, verify policy limits, and call the insurer directly to confirm the policy is active and in good standing.

Is a Certificate of Insurance enough to protect my facility?

No. A COI is a snapshot of coverage at the time of issuance. You also need an additional insured endorsement on the policy to legally extend coverage to your organization in the event of a claim.

What happens if I hire an uninsured cleaning company and an accident occurs?

Without documented insurance, financial responsibility for property damage, worker injuries, and legal costs shifts directly to the property owner, potentially resulting in significant out-of-pocket expenses or litigation.